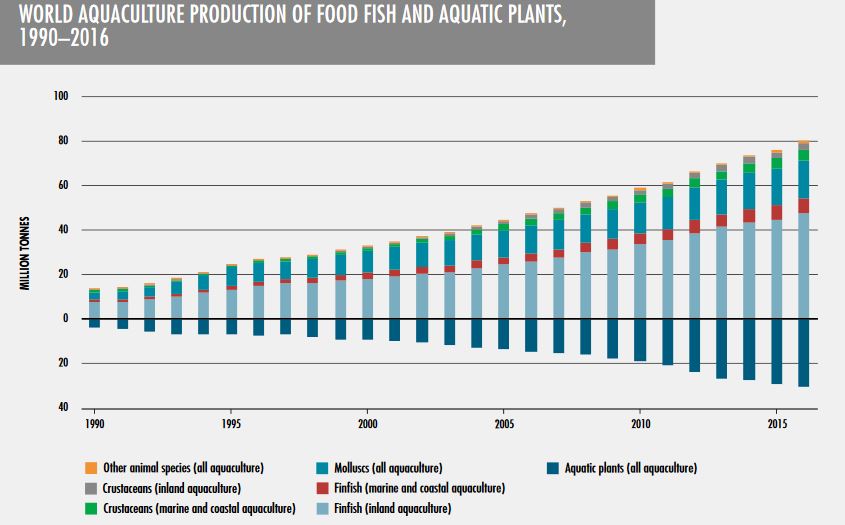

Global aquaculture and fishery resource production

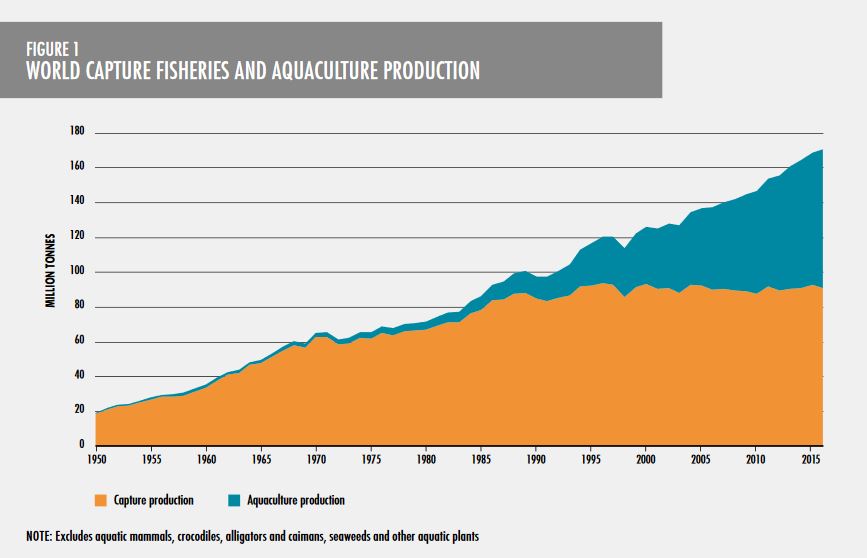

| Global seafood production has grown steadily since the mid-20th century. However, fishery catches have stagnated since the 1990s, when the production ceiling was reached at about 90 million tonnes. In contrast, aquaculture production has experienced constant growth. In 2014, the fishery catch production for human consumption equalled that of aquaculture. Aquaculture subsequently surpassed fisheries and is expected to reach 57% of total global volume in 2025, according to the FAO. Some 56 million people worked in the fisheries and aquaculture industry in 2014 and there were 4.6 million fishing vessels, 75% of which flew an Asian flag. | |

Source FAO 2016: State of World Fisheries and Aquaculture |

Fisheries

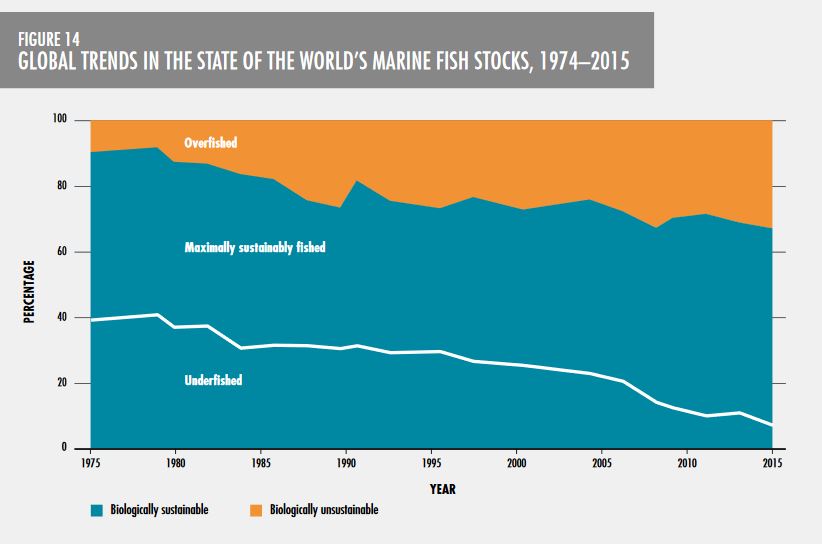

| The pressure on wild stocks may lead to this natural resource being overfished. And at a global level, the proportion of overfished stocks has risen from 10% in 1975 to 30% in 2014. Looking at European fish stocks, the recent trend has been the reverse, following the management measures in the Common Fisheries Policy (CFP) which has reduced fishery capacity through fleet decommissioning and catch restriction schemes. In fact, the number of overfished stocks in terms of the maximum sustainable yield (MSY) rose from 2 to 39 between 2005 and 2015, representing almost 60% of European fish stocks. At the same time, the number of vessels in mainland France dropped from 5,350 to 4,200 and the landed catch dropped from 600,000 to 450,000 tonnes. | |

Source FranceAgriMer 2017: The Fisheries and Aquaculture Industry in France |

| Under the European management framework, fish stocks are assessed annually by the International Council for the Exploration of the Sea (ICES) and the Scientific, Technical and Economic Committee for Fisheries (STECF). Using the available data, scientists issue their advice on the European-scale catch options for the following year, species by species and zone by zone. Their advice is then debated within the European Commission to determine the TACs (total allowable catches). The TACs are distributed to the various European countries according to the relative stability key. Those countries then distribute their national quota (giving them production rights) to their producers’ organisations. Part of the national quota is reserved for fishermen who are not affiliated with a producer organisation. In France the government manages the quota, however in most other European countries an individual transferable quota (ITQ) management system has been developed where fishermen own their production rights. Not all stocks are managed at a European level, as many coastal species are managed nationally or regionally. | |

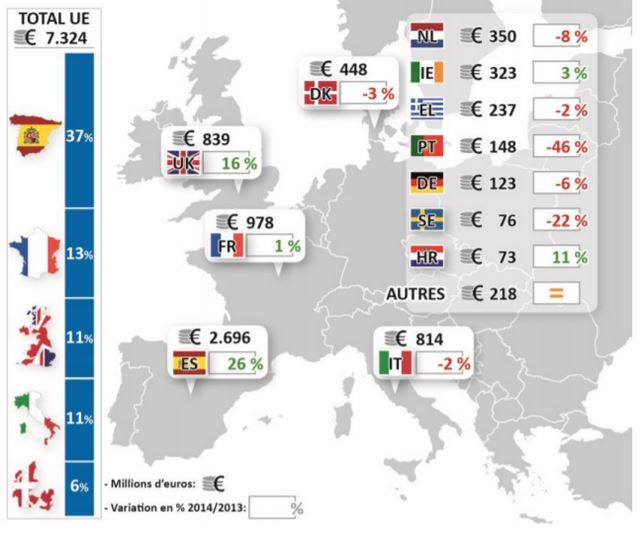

The main European producers are Spain, France, Italy and the United Kingdom.

Source EUMOFA 2016: The EU Fish Market

French fisheries are quite varied and can be categorised according to their catch method (towed/trawl gear and passive/static gear) and/or their method of vessel operation (industrial fishing, deep sea, coastal). To better understand the different fishing types, visit this website: Ifremer.

Current topics in the news are:

– Brexit: Closing British waters to European vessels already have a significant impact on the Brittany and Normandy deep sea fishing fleet which often operates in those waters.

– Fleet renewal: Ageing vessels (average age of 26 years) struggle to get replaced due to increasing fuels prices and despite of a favourable situation since 2015 with higher initial sale prices for fish .

– Vessels of the future: There are many studies currently under way to design the fishing vessels of tomorrow in order to achieve lower fuel consumption, better selectivity, greater onboard comfort for the crew, and greater catch value maximisation.

– Lack of labour: Despite attractive wages, there are few young sailors starting in the fishing profession. This means that ship owners sometimes have to engage foreign labour to compensate for that lack.

Aquaculture

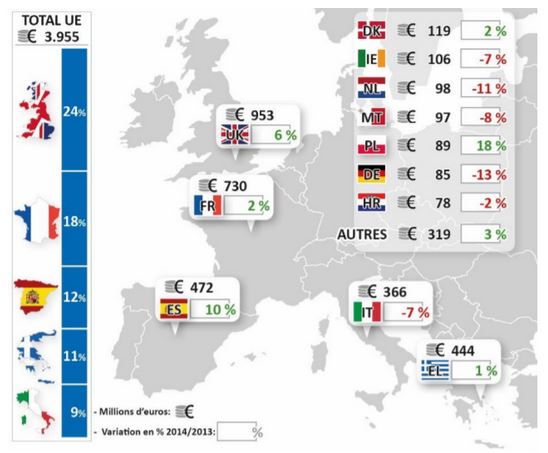

Global aquaculture is dominated by Asia, which represents nearly 90% of aquatic animal production. Production is highly diversified and involves fish, algae, molluscs and crustaceans. Aquaculture accounted for 55% of production in Asia in 2014, yet it only accounted for 18% in Europe. The main European Union producers by value are the United Kingdom, France, Greece, Spain and Italy. Bivalve molluscs (mussels, oysters and clams) figure dominantly in Spain, France and Italy. The United Kingdom primarily produces salmon, while Greece mostly produces bass and sea bream. Norway is the global leader in salmon production.

Source FAO 2016: State of World Fisheries and Aquaculture

Value of aquaculture production in 2014 (Source EUMOFA 2016: The EU Fish Market)

Farming methods are completely different from one species group to another. Fish are farmed on land in closed ponds or in the sea in cages, which require input (food). Shellfish are farmed at sea in an open space (on the ground, in pockets, on wires, on pilings, etc.) and are completely dependent on trophic input from the natural environment.

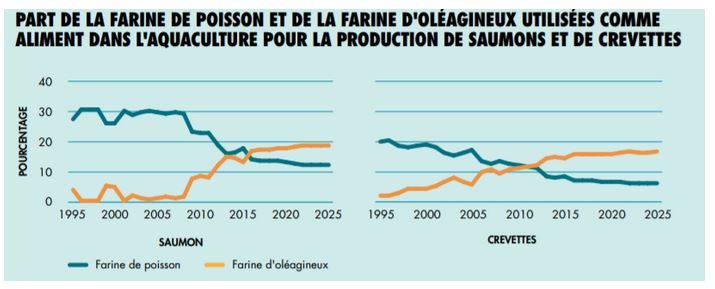

Given the increase in aquaculture production and the limit reached in farming feed fish (for processing into oil and fish meal), aquaculture feed is increasingly becoming plant-based. In fact, the portion of protein from wild fish in the feed is decreasing as it is being partially replaced by plant ingredients and, since 2017, insect meal. Another avenue of food sector research is focusing on boosting the feed conversion ratio. This coefficient expresses the quantity of feed required to produce 1kg of fish. For instance, the coefficient for salmon has dropped from 4 in the1960s (before extruded feed arrived) to 2.45 in 1985 and 1.1 in 2007 (Agreste, 2011).

Source FAO 2016: State of World Fisheries and Aquaculture

France has world-renowned expertise in new and marine aquaculture, namely in producing juvenile saltwater fish, but has not been able to significantly grow this sector despite proactive European policies. Growth is primarily hindered by conflicts of use as well as coastal property access that is complex and costly. A large portion of the juveniles produced in France are therefore transferred to other countries (namely Greece) for the fattening phase, with the added bonus of cheaper labour costs.

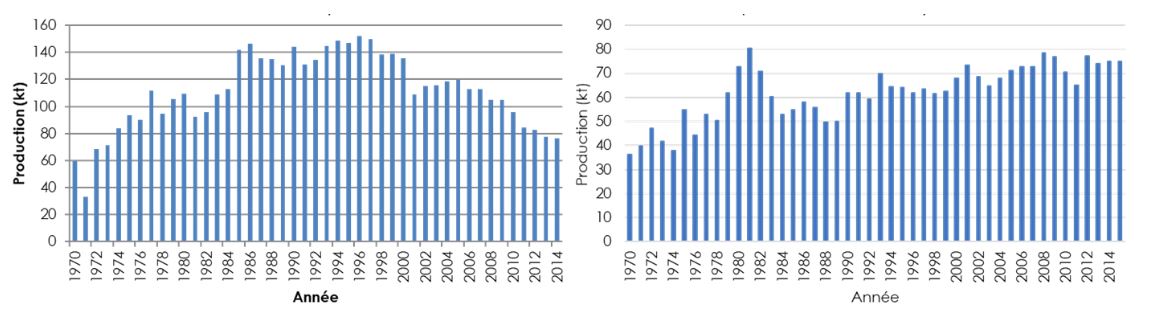

French and European oyster farming has been experiencing a major production crisis since 2000. An infectious herpes virus (OsHV-1) causes mortality amongst the juveniles and results in stock deterioration during the first year of farming. Since 2008 a variant of that herpes virus, combined with the presence of a bacteria (vibrio), has also affected adult fish. The reasons for this animal health crisis have not yet been fully explained.

Evolution of French oyster production (left) and mussel production (right) (source FAO Stats 2017)

Current topics in the news are:

– Integrated multi-trophic aquaculture: Polyculture system combining various species or species groups to create farming synergies. Waste from one species is used as a resource by another (e.g. fish, shellfish and algae).

– Aquaponics and aquaculture in peri-urban areas: Growing trend where aquaculture and plant productions can be paired up. Fish waste is used as a nutrient source for the plants. This system of water recirculation can be established in urban and peri-urban areas, as close as possible to consumption centres.

– Insects and micro-algae as protein sources: Incorporating insect meal has been authorised for aquaculture feed since July 2017. Many companies are experiencing growth in this market (Entomo Farm, Ynsect, Micronutris, etc.).